Understanding the Canada Pension Plan (CPP): What Every Working Canadian Needs to Know

In this post, we’re diving deep into one of Canada’s cornerstone retirement programs: the Canada Pension Plan (CPP). Whether you’re a salaried employee, self-employed, or an incorporated business owner, CPP is a vital part of your long-term financial planning. Here's what you need to know:

🔍 What is the Canada Pension Plan (CPP)?

The Canada Pension Plan is a government-run retirement pension designed to replace part of your income when you retire. It's a contributory, earnings-related social insurance program, meaning you pay into it during your working years and receive benefits in retirement.

Quick Facts:

Managed by: Employment and Social Development Canada (ESDC)

Available in: All provinces and territories except Québec (which runs its own Québec Pension Plan (QPP))

Eligibility: You must be at least 60 years old and have made at least one valid contribution to the CPP.

💰 How is CPP Funded?

CPP is funded by mandatory payroll contributions from both employees and employers, as well as the self-employed. Contributions are based on your annual employment income.

Contribution Rates for 2025:

Employees: 5.95%

Employers: 5.95%

Self-Employed: 11.90% (you pay both portions)

These contributions are applied to income between the basic exemption ($3,500) and the annual maximum (in 2025, the YMPE is $68,500).

For example, if you earn $60,000, your contribution (as an employee) would be 5.95% of $56,500 ($60,000 - $3500) = $3,361.75. Your employer matches that amount.

📅 When Can You Start Receiving CPP?

You can start receiving CPP as early as age 60 or as late as age 70, and the age you choose has a significant impact on your monthly payments.

🕒 Early Retirement (Age 60–64)

Your pension is reduced by 0.6% for each month you take it before age 65.

That’s a 7.2% reduction per year, or a 36% reduction if you take it at age 60.

⏳ Standard (Age 65)

No penalties or bonuses. This is considered the “base” CPP amount.

⏫ Delayed CPP (Age 66–70)

You receive a 0.7% increase per month you delay past 65.

That’s an 8.4% annual increase, or up to 42% more if you delay until age 70.

Pro Tip: If you’re still working and don’t need the money, delaying CPP can lead to significantly higher monthly payments and offer inflation protection.

👩💼 What About Self-Employed Individuals?

If you’re self-employed, you’re responsible for both the employee and employer share—a total of 11.90% of your pensionable earnings.

You report and pay this amount annually when you file your T1 tax return using the Schedule 8 (CPP Contributions).

Note: Your CPP contributions are partially tax-deductible and partially a tax credit, which can ease the cost.

🏢 Incorporated Business Owners

If you pay yourself a salary, CPP works just like any other employer-employee relationship. Your corporation remits both the employer and employee contributions.

However, if you only pay yourself through dividends, you do not pay into CPP, which means:

You avoid the contributions now.

But you won’t increase your future CPP retirement benefits.

Strategic Tip: Balancing salary and dividends can help you manage current tax efficiency and future CPP income. Speak to an accountant to find the right mix.

📈 How Much Will I Get?

The amount you receive depends on:

How much you contributed

For how many years

When you start receiving it

Maximum monthly CPP retirement pension in 2025 at age 65: ~$1,364/month Average monthly CPP (actual payments): ~$758/month

You can check your personal CPP statement through your My Service Canada Account to see your projected amount.

📊 CPP Fund Performance & Portfolio Management

You might be wondering: “Where does all that CPP contribution money actually go?” The answer is: into one of the largest and most sophisticated investment portfolios in the world, managed by the Canada Pension Plan Investment Board (CPPIB).

🏦 What is the CPPIB?

The Canada Pension Plan Investment Board (CPPIB) is an independent, professional investment organization created in 1997. Its job is to invest CPP contributions not immediately needed to pay benefits, with the goal of maximizing returns without undue risk—so CPP remains sustainable for current and future generations.

📈 How is the CPP Fund Performing?

As of March 31, 2025, the CPP Fund had:

Net assets of approximately $655 billion

10-year annualized return (net of costs): ~9.2%

A diversified, long-term approach that has outperformed many global pension funds

Despite occasional market volatility, the Fund has demonstrated strong resilience and consistent long-term growth, which is critical given its obligation to serve Canadians well into the next century.

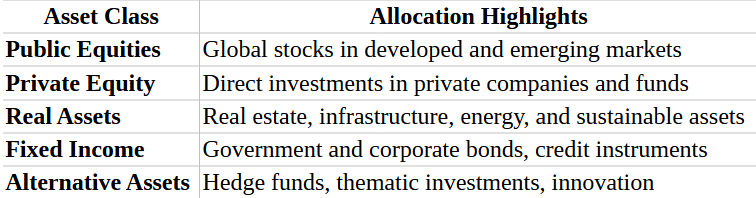

🧠 How is the Money Invested?

The CPPIB follows a globally diversified, actively managed portfolio strategy that includes:

The CPPIB’s strategy includes direct ownership stakes in major global infrastructure like toll roads, airports, data centers, and even renewable energy assets—designed to provide long-term, inflation-protected returns.

🛡 Is CPP Sustainable?

Yes. Based on the latest report from the Chief Actuary of Canada, the CPP is financially sustainable for at least the next 75 years under current contribution rates and assumptions.

This sustainability is rooted in:

The Fund’s strong long-term returns

Mandatory contributions from workers and employers

Prudent, independent portfolio management

In short: Your CPP contributions aren’t just sitting idle—they’re working for you around the world, 24/7.

🔎 Transparency and Oversight

The CPPIB is known globally for transparency, governance, and accountability. It publishes:

Quarterly and annual reports

Investment performance and strategy updates

ESG (Environmental, Social & Governance) impact disclosures

You can explore all this at www.cppinvestments.com.

🧾 Other CPP Benefits

CPP isn’t just for retirement. Other benefits include:

CPP Disability Benefit

CPP Survivor’s Pension

CPP Death Benefit (lump sum up to $2,500)

Children’s Benefits (for dependent children of disabled or deceased contributors)

📌 Final Thoughts

CPP is a powerful foundation for retirement income, but not a complete solution on its own. It’s meant to supplement personal savings, workplace pensions, and other retirement income (intended to replace about 25% of your pre-retirement income). Understanding how and when to maximize it—especially if you’re self-employed or incorporated—can significantly affect your financial future.

🛠Financial Planning with CPP

Proper financial planning means looking at the full picture—and that includes accounting for the Canada Pension Plan (CPP) alongside other key retirement savings vehicles such as Registered Retirement Savings Plans (RRSPs), Registered Pension Plans (RPPs), and Tax-Free Savings Accounts (TFSAs). While CPP provides a stable, inflation-adjusted income for life, it’s essential to supplement it with personal savings (RRSPs), employer-sponsored pensions (RPPs), and flexible, tax-free growth options like TFSAs. A thoughtful strategy coordinates when and how you draw from each source—balancing tax efficiency, income needs, and investment growth—to build a secure and sustainable retirement. Ideally, CPP acts as a foundational income layer, with your other accounts providing the flexibility and financial freedom to enjoy retirement on your terms.

If you’d like a understand how to strategically plan retirement income using CPP, RRSPs, and TFSAs, get in touch! Having an established retirement plan is essential for financial freedom and ensuring you live the lifestyle you want in retirement!